Right now, the combined household debt in the United States is a whopping $13.5 trillion. To put that figure into more relatable terms, consider the following excerpt from the Wall Street Journal: “Abe Schilling, a 33-year-old car salesman in Great Falls, Mont., said he signed up for more than five credit cards over the past year, from issuers including Capital One Financial and Discover Financial Services after he received offers in the mail. He also took out a $36,000 loan to buy a new Jeep Grand Cherokee.

Schilling, who currently rents his home, said the offers have been arriving as his credit score has improved. He previously had dozens of collections and other negative marks on his credit reports after failing to pay back bills. With a steady income and months of debt counseling behind him, Mr. Schilling says he feels confident in his ability to pay for his debts.” Unfortunately, his story is but one of millions which all culminate in this result:

consumer debt, excluding mortgages, is at its highest level ever on record. In the same vein, the average repayment period for car loans has hit a new record of 69 months each.

Consumer deficit spending is borrowed prosperity which may briefly boost the economy as a real spending stimulus, but, ultimately, leads to bankruptcy and, possibly, full on economic collapse.

Individual consumers not only eventually max out their own finances and credit, they are further burdened with rising rates.

Some other sobering statistics to quantify the current debt crisis include the estimated 78% of full-time workers in the United States who describe themselves as “living paycheck to paycheck” per a recent CareerBuilder.com survey. 56% of respondents in this survey reported their debt was already unmanageable and they didn’t see themselves as capable of getting out of debt. In 2017, BankRate.com published its own study stating approximately 57% of American citizens would be unable to handle an unexpected $500 emergency expense.

Government debt also soars, despite the current U.S. administration’s branding itself as “fiscally conservative” and promising to cut spending.

Thus far, the government has further increased spending and the national debt.

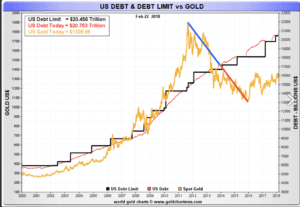

Massive U.S. military efforts and the economic collapse of The Great Financial Crisis of 2008 caused the total U.S. debt to surge from $6 trillion to $15 trillion during the almost decade long time frame between 2003 – 2012.

The federal debt is about to explode as there were no real spending cuts in the budget passed by the GOP. Furthermore, as tremendous as the U.S. military budget already is (accounting for over 80% of the budget), Congress just cleared the way for even more spending on the military in part as a roundabout way to fund a completely unnecessary border wall to appease xenophobic sensibilities. Just weeks ago, President Trump’s first budget plan projected $1T+ deficits through 2022 with total debt rising to a minimum of $25T over that same period.

At some point in the very near future, a systemic debt crisis will inevitably emerge as both private and public debt reach astoundingly high levels.

Unfortunately, the next crisis is likely to be far worse than the 2008 financial crisis and will include what are currently perceived as some of the most successful economies in the developed world.

Craig Hemke, at TFMetals.com, recently pointed out the relationship between U.S. debt and gold which adds another layer of nuance to the economic situation and role of debt. “It could be said that, beginning with The Great Financial Crisis, gold got ahead of itself. Price had consistently risen with the accumulated debt through 2009, but, by 2011, it was considerably above the established trend. In the correction that followed and ended in 2015, you might note that price fell to roughly the same distance below the established trend.”

The U.S. stock market needs a lower dollar to continue making new highs which President Trump has fully supported since it would temporarily benefit the stock market at the privilege of the already rich and at the ultimate expense of the middle and working class. These consumers are one small recession or economic hiccup away from defaulting on all their debts.

The safest prediction is the dollar will continue to fall and inflation will skyrocket over the next 3 years.

Meanwhile gold is about to gain new highs in value and enjoy a healthy rise that could eventually culminate in a parabolic spike should a real dollar crisis occur by the end of this decade.

Many industry experts are suggesting the best time to buy gold is right now. Why?

While US debt grew from $6T to $15T, the price of COMEX gold moved up from $400 to $1,800 per ounce from 2003 to 2012. However, in late 2012, the price of COMEX gold began to fall despite the over $1T QE3 program which ran from late 2012 to early 2014 as well a continuing surge in total U.S. debt from $15T to $20T.

Some now say, during the Great Financial Crisis, gold got ahead of itself and was overvalued. The price of gold had consistently risen with the accumulated debt through 2009 but, by 2011, it was considerably valued above the established trend. In the correction following through 2015, its price fell to roughly the same distance below the established trend.

It would seem that now the price pendulum has swung just as far downward in 2015 as it swung upward in 2011. Therefore, if gold was overvalued in 2011, it was equally undervalued in 2015.

What does this mean for the future of gold prices as it relates to U.S. debt?

In the months ahead, gold’s price could at least move back to the apparent median line of the accumulated U.S. debt, around $1,800 or $1,900 per ounce. Should it move to another bullish extreme as seen in 2010 – 2011, it would imply a value closer to $2,500. Another financial crisis (which appears to be looming on the horizon) could very well make this prediction a realty.

{kind=link}